Detailed, Step-by-Step NCERT Solutions for 12 Business Studies Chapter 8 Controlling Questions and Answers were solved by Expert Teachers as per NCERT (CBSE) Book guidelines covering each topic in chapter to ensure complete preparation.

Controlling NCERT Solutions for Class 12 Business Studies Chapter 8

Controlling Questions and Answers Class 12 Business Studies Chapter 8

Multiple Choice Question

For the following, choose the right answer.

Question 1.

An efficient control system helps to:

(a) Accomplish organisational objectives

(b) Boosts employee morale

(c) Judge accuracy of standards

(d) All of the above

Answer:

(d) All of the above.

![]()

Question 2.

Controlling function of an organisation is

(a) Forward looking

(h) Backward looking

(c) Forward as well as backward looking

(d) None of the above

Answer:

(c) Forward looking and backward looking function.

Question 3.

Management audit is a technique to keep a check on the performance of ……………

(a) Company

(b) Management of a company

(c) Shareholders

(d) Customers.

Answer:

(b) Management of the company.

Question 4.

Budgetary control requires the preparation of

(a) Training schedule

(b) Budgets

(c) Network diagram

(d) Responsibility centres

Answer:

(b) Budgets.

![]()

Question 5.

Which of the following is not applicable to restorability a courting.

(a) Investment center

(b) Andocentric center

(c) Profit center

(d) Cost center

Answer:

(c) Andocentric center.

Short Answer Type Questions

Question 1.

Explain the meaning of controlling.

Answer:

” An adequate control system should disclose where failures are occurring, who is responsible for them and what should be done about them.” – Konntz and O’Donnel!

Control is the last step in the Process of management because it arises need only after the other managerial steps like planning, organising and directing etc. Control is considered to,be an important means of administration since olden times. The managerial function of controlling involves the measurement of actual Performance, comparing it.

With the Planned standards and correcting deviations to ensure attainment of predetermined objectives. Thus, even though control is the last step in the Process of management, it is equally important for efficient, smooth, speedy and proper attainment of organizational goals.

![]()

Meaning and Definitions of Control : Control in context to management refers to initiating such action which make the actual process in accordance with the expected progress. It includes all those activities which direct and motivate the action to achieve the Predetermined objectives of the enterprise. It is not any means to put restrictions but it is a means through which a manager directs the behaviour of his subordinates in the desired direction by resorting to delegation and decentralisation with trust and confidence.

The modem managers believe that the meaning of control is not to establish an empire over the employees but it is a such an activity through which the activities of the. employees are directed and co-ordinated for the attainment of Pre-determined objectives. The essence of control is to see that all the activities are moving towards the attainment of desired goals or not. In other words, the meaning of control is to ensure that all the activities are Occurring according to the Plans.

Various Scholars have defined Control in different ways. Some of the important definitions are.

According to Henry Fayol, ” Control consists of verifying whether everything occurs in conformity in the plans adopted, the instruction issued and principles established. lt has for its object, to point out weakness and errors, in order to rectify them and prevent recurrence”.

- According to Joseph L. Massie,” Control is the process of taking steps to bring actual results and desired results closer together”.

- According to Philip Kotleiy “Control is the process of taking steps to bring actual result and desired result closer together.”

- According to Dale Henning, “Control is the process of bringing about Conformity of performance with planned action.”

- According to Marry Cushing Niles, “Control is the maintaining Of the balance between activities directed towards a goal or set of goals.”

- According to Billy E. Goetz, “Management Control seeks to compel events to conform to plans.”

On the basis of all the above definitions we can say that controlling includes verifying whether everything is happening properly, according to the plans, if not then finding out the obstacles and making efforts to remove them. For this purpose, the actual work progress is-measured and compared to the standard already determind in order to find out the deviations and remove such deviations by taking corrective action.

![]()

Question 2.

“Planning is looking ahead and controlling is looking back”. Comment.

Answer:

Planning is done always for the future. It is a well thought outline of the future events. According to George Terry, “Planning is oriented to and requires a feeling for the future. It is an investment of thought and time in the present for reaping the benefits in future. Some people believe’ that planning is unearthing the things for a better future.” It is called looking ahead because a well thought procedure is following in the future.

According to Allen, “Plan is a trap which is laid down to catch the future.” Thus it is clear that planning involves making estimates for the future, the more correct the estimates the more successful would.be the PlAnswer:Thus it is true that planing is looking in to the future.

It contrast to planning, control is called a looking back because a manager makes a comparison with the laid down standards Only after certain activity has been performed is compared with the- predetermined standards. Since both these activities have been already performed hence to compare them is in fact looking back. Looking back means, evaluating the work or performance which has already been done.

The thought of looking back in context to control is partially – correct. Control is not only looking back but also looking ahead. This has two reasons – First, the corrective action which is an important part of control is one of the measures of looking ahead. Second a good control system is the one which informs about the deviations even before their occurrence and prevents their reoccurrence. In other words, control is not only a remedial action but also a preventive action which reduces the possibilities of deviations.

Question 3.

“An effort to control everything may end up in controlling nothing”*. Explain. ‘ *

Answer:

Management control is that process of ensuring that actual activities conform to planned activities. Controlling helps in accomplishing organizational goals, judging accuracy of standards, ensuring different utilization of resources, but an effort to control everything sometimes create problems in controlling.

Controlling, suffers from certain limitations. An organization has no control over external function The control system of an organization may face resistance from its employees. Controlling also looses its effectiveness when standards cannot be defined in quatitative terms which makes the measurement of performance arid their comparison with standards a difficult task. Controlling is a costly affair as it involves lot of expenditure, time and effort. A small enterprise cannot afford to control an expensive control system.

Control is often resisted by employees. They see it as a curb to their freedom. External factors like government policies, technological changes, competition etc. cannot be controlled. Therefore, an effort to control everything is not justified. Overall organizational objectives should be kept in mind while controlling the activities in an organization.

![]()

Question 4.

Write a short note on budgetary control as a technique of managerial control.

Answer:

Budgetary control : Budgetary control is a system of management control in which all operation are planned ahead in the form of budgets and actual results are compared with budgetary Satandards and the necessary actions are taken to ensure attainment of organisational objectives.

According to G.R. Terry “Budgetary control is a process of comparing the actual results with the corresponding budget data in order to approve accomplishments or to remedy differences by either adjusting the budget estimate or correcting the cause of the differences”.

Thus, in budgetary control first of all, the budgets for all the activities of the Organisation are prepared, then the actual result are compared with these budgets and if any diviations are found on comparison then the reasons for them are located.

If the deviations are able to be remove on correcting the reasons then the same is done otherwise necessary amendements are made in the. Plans Before studying budgetary control in detail it is necessary to understand the three related terms : budget, budgeting and budgetary control Budget.

A budget’is a financial or quantitative expression of the plan of a action to be presumed in a definite future period. In other words, a budget presents financial or quantitative details of what is to be done in future.

![]()

Budgeting.

The process of preparing a budget is called budgeting. In other words, the process of collecting the necessary information and data and presenting them in the form of a statement in numerical terms is called budgeting.

Budgetary control

Budgetary control is a process of exercising control through budgets. It is a system of comparing actual result with the budgets and taking necessary steps to correct the deviations.

Characteristics of Budgetary Control

The main characteristics of budgetary control are as follows

(i) Process of Comparing : It is a process of comparing the actual results with the estimated figures.

(ii) Finding out the Deviations : On comparing the actual results with the estimated ones, certain deviations are found. Steps are taken to find out the causes for. such deviations.

(iii) Taking corrective action : After finding out the causes for deviations, corrective action is taken to remove the cause of such deviations.

(iv) Budgets are based on Forecasts : The budgets are the estimates which are based on scientific forecasts.

(v) Separate Budgets are prepared for all the Departments.

Different budgets are prepared for all the Departments or activities and later all these budgets^are included in the form of a common budget for the entire enterprise, which is called a master budget.

Requisites for success of Budgetary control . To make the budgetary control successful following factors must be considered.

(i) Full Support : The budgetary control must receive full support of the top executives of the enterprise.

(ii) Full participation : The budgetary control can be. successful only when all the executives associated with its emplementation actively participate in its formation.

(iii) Sound Organisation structure : The structure of the organisation should be according to the budget arrangements so that the specific responsibilities can be handed over to specific people.

(iv) Clear Defination of Budget authority and Responsibility: The authority must and responsibility of making and executing the budget must be clearly defined.

(v) Flexibility : A budget should be flexible enough to be changed according to . the changes in the situation.

(vi) Motivation : For the success of budgetary control it must have arrangement for rewarding the efficient employee and punishing the inefficient ones.

(vii) Feed back system : There must be proper arrangements of transmission of the progress report of various departments to the budget official. Also the opinion and suggestions of various officers responsible for implementing the budget must also reach the budget officials. This helps in bringing about improvements in the budget in the future.

(viii) Adequate Time : The decisions of the success or failure of the budgetary control cannot be taken in short time. It can be taken only after the passage of some time.

![]()

Question 5.

Explain how management audit serves as an effective technique of controlling.

Answer:

Management Audit : The quality of management is the main determinant for the success or failure of an organisation. Management audit focuses attention on evaluation of quality of management.

It is an independent and critical examination of total management process of planning, organising, staffing, directing and controlling. It helps in locating the deficiencies in the performance of these managerial functions and advice the top management for necessary adjustments in order to make the organisation more effective.

Management audit is nothing but an extension of financial audit and its functions begin from where the functions of financial audit end. According to Koontz and O’ Donnell, management audit, “Auditing the quality of managers through appraising them as individual managers and appraising the quality of the total system of managing in an enterprise.”

Thus, we can say that the main objectives of management audit is to conduct a systematic and unbiased analysis and evaluation of a entire management system. It makes a critical analysis of the organisational structure, its various departments, Plans of management, Policies, work-procedures, use of human and physical resources and various other achievements and failures with a view to determine the afficiency of the managers. So as to bring about improvement in them.

Procedure of Management Audit : The following Procedure is normally followed for conducting management audit.

(i) Preliminiary Decisions : First of all, the board of directors of the organisation or the managing director decides about the objectives of the management audit, what shall be included in it, when it shall be done and who shall be its auditors.

(ii) Audit : After making the initial decisions the actual work of the management audit begins. It includes various activites like determination of the’sources and means of information, making the audit Programme, inspection of necessary records and reports, interviewing the managers, making surveys, inspection of the organisation structure, inspection of various techniques of motivation, communication and control, considering their suitability, reporting the difficulties etc. Apart from this, he judges the quality of managerial decisions taken in various field of management.

![]()

(iii) Critical Appraisal : After obtaining all the necessary informations, the management auditor makes a critical evaluation of it and tries, to find out unneccessary activities, differentiate between the activities which are required and which are not required for the achievement of objectives, what are the various problem related with the implementation of various Policies, Procedures and decisions.

(iv) Suggestions for improvement : After making such analysis the auditor suggests the remedial actions which are based on his experience, suggestions of various executives and the directions of the top executives to bring about improvement in the management of the company.

Long Answer Type Questions

Question 1.

Explain the various steps involved in the Process of control.

Answer:

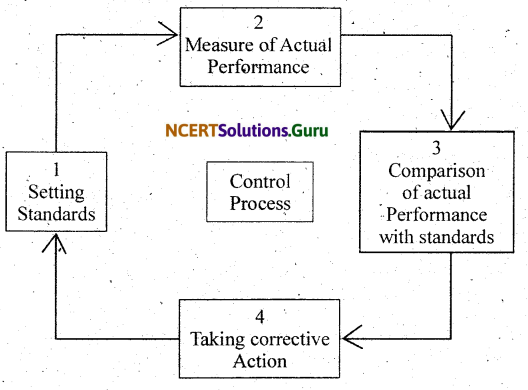

Control Process : The Process of control involves the setting of standards comparison of actual result with the standards, detection and correction, of the deviations if any.

Thus, the Process of Control involves four steps:-

- Setting standards

- Measurement of Actual Performance.

- Comparison of actual Performance with the standards and calculating Deviations.

- Taking corrective Action.

1. The Process of control can be presented by way of diagram as follows

Setting Standards : The first step in the control Process is the setting up of control standards. Standards Present the criteria against which actual Performance is measured. Standards serve as the bench marks because they reflect the desired results or Performance. The standard can be laid down in terms of physical terms like quantities of the Product, labour-hours, units of service, speed, etc. or in monetary terms like sales value, costs, capital espenditure or Profit etc.

These standards must be easily attainable through the available capability and resources. The standard must also be according to the Plans of Process of the enterprise. While setting the standards the managers should keep in mind that they are

- Simple and easily attainable

- definite

- measurable

- according to the objectives

- flexible

- timely and

- economical.

To make standrds effective it should be ensured that different standards are laid down for different responsibility centers so that it becomes easier to motivate the employees of different centers.

The extent of deviations which shall be considered as normal should also be laid down because some deviations between the standards and actuals are inevitable. Thus, the limits up to which deviations shall be tolerated must be established. such limits must neither be too high nor too low.

![]()

2. Measurement of actual Performance : The next step in the Process of Control is the measurement of actual Performance. While measuring actual Performance it should be ensured that

- The date of Progress should be prepared regularly and constantly.

- So far as possible measurement should be done during the course of Performance.

- The figures of date of measurement should be accurate and reliable.

- Report regarding important deviations should reach the manager very quickly so that corrective action may be taken immediatey.

While Preparing the report maximum emphasis should be given to the deviations which are highly important because the top managers do not have must time and they are expected to concentrate only on important deviations. The managers may not pay need to the deviations which are with in the prescribed limits.

3. Comparison of Actual Performance with Standards and Calculations of Deviation . The third major step in the control.Process involves the comparison of actual Performance with the Standard Performance. Such comparison will reveal the deviations between actual and desired results. Steps are taken to find out the reasons for the deviations. There could be many reasons for the deviations like:

- Setting of wrong standards : Like wrong estimates of cost of production, sales, Profits etc.

- General Hurdles : Like short supply of raw materials, breaking of machines etc.

- Change in circumstances : Like entry of new competitors in the market, change in demand, fashion etc.

- Human Causes : Inefficiency in completing the work by different individuals or groups.

Here, managers should see that they concentrate only on major deviations because small deviation can be coincidental. Thus they need not be given much attention.

From the analytical viewpoint deviations can be divided into following two categories.

(i) Controllable Deviations : Ones which can be controlled, and

(ii) Uncontrollable Deviations : Ones which cannot be controlled but can be reduced with the help of good system of forecasting. For example entry of various competing firms in the market is an uncontrollable deviation. Corrective actions can rectify only the controllable deviations.

4. Taking Corrective Action

The final step in the control Process is taking corrective action. Actually corrective action is the soul of controll Process. Its main aim is to help in making actual process in accordance with the expected Progress. It includes two types in activities.

- To remove deviations in actual Progress.

- To Prevent reocurrence of the deviations.

The managers should consider four things while taking corrective actions.

- Corrective actions should be undertaken immediately

- Corrective actions should be based upon a careful inquiry into causes of deviations and not on any guesswork or hypothetical ideas.

- Corrective actions should be compatible with the Psychology of the related employees.

- Corrective actions should be initiated by the managers at the same level at which the deviations are recorded.

![]()

Question 2.

Explain the techniques of managerial control.

Answer:

Techniques of Managerial Control

The various techniques of managerial control may be classified in to two broad categories

(i) Traditional techniques and

(ii) Modern techniques.

(i) Traditional Techniques : Tradinational Techniques are those which have been used by the companies for a long time now. However, these techniques have not become obsolete and are still being used by companies. These include:

a. Personal observation

b. Statistical reports

c. Breakeven analysis

d. Budgetary control

(ii) Modern techniques : Modem Techniques of controlling are those which are of recent origin and are comparetively new in management literature. These techniques provides a refreshingly new thinking on the ways in which various aspects of an organisation can be controlled. These include

- Return on investment

- Ratio Analysis

- Responsibility accounting

- Management audit

- PERT and CPM

- Management information system.

Traditional Techniques

Personal Observation : This is the most traditional method of control. Personal observation enables the manager to collect first hand information. It also creates a Psychological pressure on the employees to perform well as they are aware that they are being observed personally on their job. However, it is a very time-consuming exercise and cannot effectively be used in all kinds of jobs.

Statistical Reports : Statistical Analysis in the form of averages, percentages, ratios, correlation, etc. Present useful information to the managers regarding performance of the Organisation in various areas. Such information when presented in the form of charts, graphs, tables, etc. enable in managers to read them more easily and allow a comparison to be made with performance’ in previous periods and also with the benchmarps.

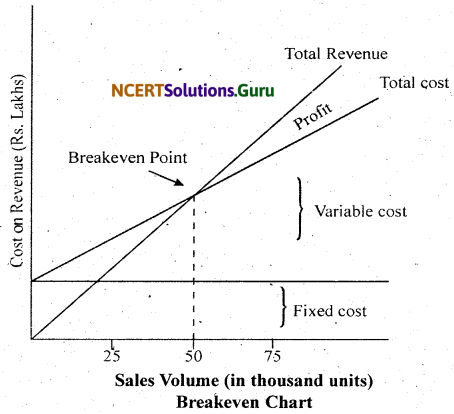

Breakeven Analysis : Breakeven analysis is a technique used by managers to study the relationship between costs, volume and profits. It determines the probable profit and losses at different levels of activities. The sales volume at which there is no profit, no loss is known as breakeven point. It is a useful technique for the managers as it helps in estimating profits at different levels of activities.

Figure shows breakeven chart of a firm. Breakeven Point is determined by the intersection of Total Revenue and Total Cost curves. The figure show that the firm will break even at 50,000 units of output. At this point, there is no profit no loss. It is beyond this point that the firm will start earning profits.

Breakeven Point can be calculated with the help of the following formula

Breakeven Point = \(\frac{\text { Fixed Costs }}{\text { Selling Price Per unit – Variable cost per unit }}\)

Breakeven analysis helps a firm in keeping a close check over its variable costs and determines the level of activity of at which the firm can earn its target Profit.

Budgetary Control

Budgetary control is a technique of managerial control in which all operations are planned in advance in the form of budgets and actual results are compared with budgetary standards. This comparison reveals the necessary actions to be taken so that organisational objectives are accomplished.

![]()

Budgeting offers the following advantages.

1. Budgeting focuses on specific and time-bound targets and thus, helps in attainment of organisational objectives.

2. Budgeting is a source of motivation to the employees who know the standards against which their performance will be appraised and thus, enables them to perform better.

3. Budgeting helps in optimum utilization of resources by allocating them according to the requirements of different departments.

4. Budgeting is also used for achieving coordination amount different departments of an organisation and highlights the interdependence between them. For instance, sales budget cannot be prepared without knowing prodution programmes and schedules.

5. It facilities management by exception by stressing on those, operations which deviate from budgeted, Standards in a significant way. However, the effectiveness of budgeting depends on how accurately estimates have been made about future. Flexible budget should be prepared which can be adopted it forecasts about future turn out to be different, especially in the fact of changing environmental “forces, managers must remember that budgeting should not be viewed as an estimate but a means to achieve organisational objectives.

Modern Techniques

Return on Investment : Return on Investment (ROI) is a useful technique which provides the basic yardstick for measuring whether or not invested capital has been used effectively for generating resonable amount of return. ROI 1 can be used to measure overal 1 Performance of the organisation or of its individual departments or divisions. It can be calculated as under.

\(\mathrm{ROI}=\frac{\text { Sales }}{\text { Total Investment }} \times \frac{\text { Net Income }}{\text { Sales }}\)

Net Income before or after tax may be used for making comparisons. Total investment includes both working as well as fixed capital invested in business. According to this techniques, ROI can be increased either by increasing sales volume proportionately more than total investment or by reducing total investment without having any reductions in Sales Volume.

ROI provides top management an effective means of control for measuring and comparing performance of different departments. It also permits departmental managers to find out the problem which affects ROI in ait advers manner.

Ratio Analysis :

Ratio Analysis refers to analysis of financial statements through computation of ratios. The most commonly used ratios used by organisations can be classified into the following categories.

1. Liquidity RatiosLiquidity ratios are calculated to determine short-term solvency of business. Analysis of current position of liquid funds determines the ability of the business to pay the amount due to its state holders.

2. Solvency Ratios : Ratios which are Calculated to determine the long term Solvency of business are known as solvency Ratios. Thus, these ratios determine the ability of a business to service its indebtedness.

3. Profitability Ratios These ratios are calculated to analyse the Profitability Position of a business. Such ratios involve analysis of Profits in relation to sales or funds or capital employed.

4. Turnover RatiosTurnover ratios are calculated to determine the efficiency of operations based on effective utilisation of resources higher turnover means better utilisation of resources.

Responsibility Accounting :

Responsibility Accounting is a system of accounting in which different Section, divisions and departments of an organisation are set up as ‘Responsibility Centers. The head of the center is responsible for achieving the target set for his center.

Responsibility centers may be of the following types.

1. Cost Center:- A cost or expense center is a segment of an organisation in which managers are held responsible for the cost incurred in the center but not for the revenues. For example, in a manufacturing organisation, production department is classified as cost center.

2. Revenue Center : A revenue center is a segment of an organisation which is primarily responsible for generating revenue. For example, marketing departments of an organisation may be classified as a revenue center.

3. Profit Center : A Profit center is a segment of an organisation whose manager is responsible for both revenues and costs. For example, repair and maintenance departments of an organisation may be treated as a profit center if it is a allowed to bill other production departments for the services provided to them.

4. Investment Center : An investment center is responsible not only for profits but also for investments made in the center in the form of assets. The investment made in each center is separately ascertained and return on investment is used as a basis for judging the performance of the center.

Management Audit : Management audit refers to systematic appraisal of the overall v Performance of the management of an organisation. The purpose is to review the efficiency and effectiveness of management and to improve its performance in. future periods. It is helpful in identifying the deficiencies in, the Performance of management functions. Thus, Management audit may be defined as functioning, performance and effectiveness of management of an organisation.

PERT and CPM

PERT (Programme Evaluation and Review Techniques) and CPM (critical Path method) are important Network techniques useful in Planning and Control. These techniques are especially useful for planning, scheduling and implementing time bound projects involving performance of a variety of complex, diverse and interrelated activities.

These techniques deal with time scheduling and resource allocation, for these activities aim at effective execution of Projects with in given time schedule and structure of costs.

The steps involved in using PERT/CPM are as follows.

1. The Project is divided into a number of clearly indentifiable activities which are then arranged in a logical sequence.

2. A Network diagram is prepared to show the sequence of activities, the starting point and the termination Point of the Projects.

3. Time estimates are prepared for each activitiy. PERT requires the preparation of three time estimates – optimistic (or shotest time), pressimistic (br longest time) and most likely time. In CPM only one time estimate is prepared. In addition, CPM also requires making cost estimates for completion of Project.

4. The longest path in the network is identified as the critical path. It represents the sequence of those activities which are important for timely completion of Project and where no delays can be allowed without delaying the entire Projects. If required, the Plan is modified so that execution and timely completion of project is under control. PERT and CPM are used extensively in areas like ship- building, construction projects, aircraft manufacturing etc.

![]()

Question 3.

Explain the importance of controlling in an Organisation. What are the problems faced by the organisation in implementing an effective control system?

Answer:

Importance of Controlling : Control is an indispensable function of Management. Without Control the best of Plans can go away. A good control system helps an organisation in the following ways.

1. Accomplishing Organisational goals : The controlling function measures progress towards the organistional goals and brings to light the deviations, if any, and indicates corrective action. It thus, guides the Organisation and keeps it on the right track so that organisation goals might be achieved.

2. Judging accuracy of standards : A good control system enables management to verify whether the standards set are accurate and environment and helps to review and revise the standards in the light of such changes.

3. Making efficient use of resources : By exercising control, a manager seeks to reduce wastage and spoilage of resources. Each activity is performed in accordance with predetermined standards and ndrms. Thus ensures that resources are used in the must effective and efficient manner.

4. Improving employee motivation : A good control system ensures that employees know well in advance what they are expected to and what are the standards of performance on the basis of which they will be appraised. It, thus, motivates them and helps them to give better performance.

5. Ensuring order and discipline : Controlling creates an atmosphere of order and discipline in the organisation. It helps to minimize dishonest behaviour on the part of the employees by keeping a close check on their activities. Exhibit – It explains how an important export company was able to track dishonest employees by using computer monitoring as a part of their control system.

6. Facilitating coordination in action : Controlling provides direction to all activities and efforts for achieving organisational goals. Each department and employee is governed by predetermined standards which are well coordinated with one another. This ensures that overall organisational objectives are accomplished.

Limitation of Controlling : Although controlling is an important function of management, it suffers from the following limitations.

1. Difficulty in setting quatitative standards : Control system loses its effectiveness when standards connot be defined in quantitative terms. This makes measurement of performance and th,eir comparison with standards a difficult task. Employee moral, job satisfaction and human behaviour are such areas where this Problem might arise.

2. No Control on external factors : An enterprise cannot control external factors such as government policies, technological changes, competition etc.

3. Resistance from employees : Control is often resisted by employees. They see it as a curb to their freedom. For instance employees might object when they are kept under a strict watch with the help of CCTVs.

4. Costly affair : Control is a costly affair as it involves a lot of expenditure, time and effort. A small enterprise cannot effort to install an expensive control system. It cannot justify the expenses involved. Managers must ensure that the costs of installing and operating a control system should not exceed the benefits derived from it.

Question 4.

Discuss the relationship between planning and controlling.

Answer:

Control is Aimless without planning : Control is impossible without planning. Planning helps to determine which department and which individuals have to achieve what objectives, within how much time and at what costs. Thus, control becomes more effective because the,manager become aware and able to compare the actual progress of. each related department and individual with the desired standards.

If the actual progress is less than the desired standard then the managers cannot only analyse the reasons for it but also determine the responsibility of it. In the absense of planning the managers do not have such scientific standards against which they can evaluate the progress of the employees. That is why planning is said to be the life blood of control.

![]()

From the above mentioned discussion it is clear that the functions of control and planning are so must interlinked with each other that it is very difficult to seperate the two and one is incomplete without the other. Newman and Warren have rightly said, “Planning without corresponding control are apt to hollow hopes.”Planning without control is Meaningless exercise, Control is Aimless without Planning

Control and planning are closely related to each other. Planning is meaningless without control and control is aimless without. planning. Planning without control is merely a pipe dream or wishful thinking. The best .laid plans may go astray in the absense of an adquate control system. Planning is the basis of control. Control implies the existence of certain standards against which the actual results may be evaluated. These standards are.formed only on the . basis of planning.

(i) Planning without control is Meaningless Exercise : Through planning we decide as to what is to be done in the future. In it objectives are laid down for the desired future and necessary methods to achieve them are decided, It is a process through which the organisations bring about a harmony in their objectives and business oppurtunities with their available resources.

If plans are not executed properly then they shall remain a mere wishful thinking and will lead to misuse of the organisational resources and failure to achieve the organisational objectives. Thus planning becomes successful only when it is executed effectively. For this, control is essential.

If the activities are not performed according to plans than the reasons for the same are detected and corrective actions are taken immediately to remove then. Thus, planning becomes meaningless in the absence of control.

Application Type Questions Answers

Following are some behaviours that you and others might engage in on the job. For each item, choose the behaviour that management must keep a check to ensure an efficient control system.

Question 1.

Biased performance appraisals :

Answer:

The behaviour of immediate superior to subordinate is undesirable as the work of performance appraisal by immediate superior or boss should be made on merit and that must be free from any biasness.

Question 2.

Using company’s supplies for personal use :

Answer:

Using company’s supplies for personal use is an objectionable behaviour of personnel incharge of organizational supplies of materials etc. Such practices should be curbed immediately when comes to notice of the immediate senior. Manager should sack such erring official immediately or be transferred to other jobs where such type of check be maintained.

Question 3.

Asking a person to violate company’s rules :

Answer:

Asking a person to violate company’s rule is against the organizational norms and the behaviour of such employee is dangerous for organizational growth and progress. Management should ensure that strict observance of organization’s rules and policies by every employee. With the help of effective control, an atmosphere of order and discipline be created, which helps to minimise dishonest behaviour on the point of employee by keeping a close check on their activities.

Question 4.

Calling office to take a day off when one is sick :

Answer:

Calling office to take a day off when one is sick is a behaviour responsible to create an atmosphere pf restlessness in the minds of employee who worked sincerely and committedly. Controlling provides coordination among all employers and departments.

Question 5.

Overlooking boss’s error to prove loyalty :

Answer:

Overlooking boss’s error to prove loyality is a behaviour of flattering of the superior. Such type of personal or employee and their behaviour is a real danger to the organization and also create a stigma to the knowledge and capabilities of the superior. Management should make a rational judgement between wrong and write. Management should keep himself/herself of the above such things and make sure that such behaviour will not repeat in future.

Question 6.

Claiming credit for someone else’s work :

Answer:

Claiming credit for someone else’s work is a human distorted psychological behaviour. Management should take stern action against such employee. Management should also empower employees by giving them the responsibility and accountability for their performance, including the authority to halt production to correct the problems. He should also create work cells, that is within the company that manage their production with limited supervision.

Question 7.

Reporting a violation on noticing it:

Answer:

Reporting a violation on noticing it is also a positive behaviour and should not be avoided. Management must ensure that any violation of rules and, procedure in the organization not be tolerated and reported to the immediate superior.

![]()

Question 8.

Falsifying quality reports :

Answer:

Falsifying Quality Reports hinder to achieve the desired results. In such situation, measurement of actual perforfnance with the standard performance will never be possible. Management should pinpoint such officials and take necessary action so that such, occurrences will not be repeated in future.

Question 9.

Taking longer than necessary to do the job .

Answer:

Taking longer than necessary to do the job will make the controlling a costly affair as it involves a lot of expenditure time and effort. A small organization cannot afford such control system. The management should ensure that goals should be achieved within a stipulated time and costs of installing a control system should not exceed the benefits derived from it.

Question 10.

Setting standards in consultation with workers. You are also required to suggest the management how the undesirable behaviour can be controlled.

Answer:

Setting standards in consultation with workers is a desirable behaviour for better performance and control. At the time of setting standards manager should try to set standard’s in preuse quantitative terms which makes comparison with actual performance easier.

Case Problem -1

A company ‘M’ limited is manufacturing mobile phones both for domestic Indian market as well as for export. It had enjoyed a substantial market share and also had a loyal customer following. But lately it has been experiencing problems because its targets have not been met with regard to sales and customer satisfaction. Also mobile market in India has grown tremendously and new players have come with better technology and pricing. This is causing problems for the company. It is planning to revamp its controlling .system and take other steps neccessary to rectify the problems it is facing.

Question 1.

Identify the benefits the company will drive from a good control system.

Answer:

It will help in accomplishing its goals and will help in judging accuracy of standards. It will ensure efficient utilization of resources etc.

Question 2.

How can the company relate its planning with control in this line of business to ensure that its plans are actually implemented and targets attained.

Answer:

A good control system ensures that employees knew well in advance what they expected to do. It will create an atmosphere of order and discipline. When its employees know about the plan well in advance they will achieve their goal successfully.

Question 3.

Give the steps in the control process that company should follow to remove the problems it is facing.

Answer:

There are five main steps that company should follow

1. Setting performance standards

2. Measurement of actual performance

3. Comparison of actual performance with standards

4. Analysis deviation

5. . Taking corrective actions

4. What techniques of control can the company use?

Answer:

Company should use Traditional Techniques because it involves.

1. Personal observation

2. Statistical reports

3. Breakeven analysis

4. Budgetary control.

![]()