Detailed, Step-by-Step NCERT Solutions for 11 Accountancy Chapter 1 Introduction to Accounting Questions and Answers were solved by Expert Teachers as per NCERT (CBSE) Book guidelines covering each topic in chapter to ensure complete preparation.

Introduction to Accounting NCERT Solutions for Class 11 Accountancy Chapter 1

Introduction to Accounting Questions and Answers Class 11 Accountancy Chapter 1

Test Your Understanding – I

Complete the following sentences with appropriate words :

(a) Information in financial reports is based on ……………. transactions.

(b) Internal users are the …………….of the business entity.

(c) A would most likely use an entities financial report to determine whether or not the business entity is eligible for a loan.

(d) The Internet has assisted in decreasing the …………. in issuing financial reports to users.

(e) …………….users are groups outside the business entity, who uses the information to make decisions about the business entity.

(f) Information is said to be relevant if it is …………

(g) The process of accounting starts with and ends with …………

(h) Accounting measures the business transactions in terms of ………….. units.

(i) Identified and measured economic events should be recording in ……………. order.

Answer:

(a) economic

(b) management/employees

(c) creditor

(d) time-gap

(e) external

(f) free from bias

(g) identifying the transactions, communicating information

(h) monetary

(i) chronological

![]()

Test Your Understanding – II

You are a senior accountant of Ramona Enterprises Limited. What three steps would you take to make your company’s financial statements understandable and decision useful?

1. ……………

2. ……………

3. ……………

[Hint : Refer to qualitative characteristics of accounting information] .

Answer:

1. Reliability i.e. verifiability, faithfulness, neutrality

2. Relevance i.e. timeliness

3. Understandability and comparability.

Test Your Understanding – III

Which stakeholder group ……. Would be most interested in

…………….. (a) the VAT and other tax liabilities of the firm .

…………….. (b) the potential for pay awards and bonus deals

…………….. (c) the ethical or environmental activities of the firm

…………….. (d) whether the firm has a long-term future

…………….. (e) profitability and share performance

…………….. (f) the ability of the firm to carry on providing a service or producing a product.

Answer:

(a) Government and tax-authorities

(b) Management

(c) Social responsibility groups or NGO

(d) Lenders

(e) Suppliers and creditors

(d) Customers

![]()

Test Your Understanding – IV

Tick the Correct Answer

Question 1.

Which of the following is not a business transaction?

(a) Bought furniture of Rs. 10,000 for business

(b) Paid for salaries of employees Rs. 5,000

(c) Paid sons fees from her personal bank account Rs. 20,000

(d) Paid sons fees from the business Rs. 2,000

Answer:

(c) Paid sons fees from her personal bank account Rs. 20,000

Question 2.

Deepti wants to buy a building for her business today. Which of the following is the relevant data for his decision?

(a) Similar business acquired the required building in 2000 for Rs. 10,00,000

(b) Building cost details of 2003

(c) Building cost details of 1998

(d) Similar building cost in August, 2005 Rs. 25,00,000

Answer:

(a) Similar business acquired the required building in 2000 for Rs. 10,00,000

Question 3.

Which is the last step of accounting as a process of information?

(a) Recording of data in the books of accounts

(b) Preparation of summaries in the form of financial statements

(c) Communication of information

(d) Analysis and interpretation of information

Answer:

(c) Communication of information

Question 4.

Which qualitative characteristics of accounting information is reflected when accounting information is clearly presented?

(a) Understandability

(b) Relevance

(c) Comparability

(d) Reliability

Answer:

(a) Understandability

![]()

Question 5.

Use of common unit of measurement and common format of reporting promotes;

(a) Comparability

(b) Understandability

(c) Relevance

(d) Reliability

Answer:

(a) Comparability

Test Your Understanding – V

Mr. Sunrise started a business for buying and selling of stationery “ with Rs. 5,00,000 as an initial investment. Of which he paid Rs. 1,00,000 for furniture. Rs. 2,00,000 for buying stationery items. He employed a sales person and clerk. At the end of the month he paid Rs. 5,000 as their salaries. Out of the stationery bought he sold some stationery for Rs. 1,50,000 for cash and some other stationery for Rs. 1,00,000 on credit basis to Mr. Ravi. Subsequently, he bought stationery’ items of Rs. 1,50,000 from Mr. Peace. In the first week of next month there was a fire accident and he lost Rs. 30,000 worth of stationery. A part of the’machinery, which cost Rs. 40,000 was sold for Rs. 45,000.

From the above, answer the following :

1. What is the amount of capital with which Mr. Sunrise started business.

2. What are the fixed assets he bought?

3. What is the value of the goods purchased?

4. Who is the creditor and state the amount payable to him?

5. What are the expenses?

6. What is the gain he earned?

7. What is the loss he incurred?

8. Who is the debtor? What is the amount receivable from him?

9. What is the total amount of expenses and losses incurred?

10. Determine if the following are assets, liabilities, revenues, expenses or none of the these: sales, debtors, creditors, salary to manager, discount to debtors, drawings by the owner.

Answer:

1. RS. 5,00,000

2. Rs. 1,00,000

3. Rs. 2,00,000

4. Mr. Peace, Rs. 1,50,000

5. Rs. 5,000 (salaries)

6. Rs. 5,000

7. Rs. 30,000

8. Mr. Ravi, Rs. 1,00,000

9. Rs. 35,000

10. Assets – Debtors

Liabilities – Creditors

drawings by the owner Revenue – sales

Expenses – salary to manager, discount to debtors.

Short Answer Type Questions

Question 1.

Define accounting?

Answer:

Accounting – Defined

“Accounting is the art of recording classifying and summarising in a significant manner and in terms of money: transactions and events which are, in part at least, of financial character, and interpreting the results there of ”

– Committee on terminology of the American Institute of Certified Public Accountants

“Accounting is the science of recording and classifying business 1 transactions and events, primarily of a financial character, and the art of making significant summaries, analysis and interpretations of those transactions and events and communicating the results to persons who must make decisions or form judgement ”. – Smith and Ashbourne

![]()

Accounting is a larger concept than book-keeping. Besides the function of book-keeping, accounting involves summarizing, analyzing, interpreting the financial statements and communicating the results to the users of these statements. Accounting is the language of business; it means that an enterprise communicates with the outside world, including the proprietors, through accounting statements. One cannot understand the affairs of an enterprise unless the enterprise prepares financial statements intelligibly.

Question 2.

State what is the end product of financial accounting?

Answer:

The basic purposes of financial accounting are the following :

- Calculating the result of business operations.

- Ascertaining the financial position.

- Communicating the information to the users.

To calculate the results of operations : To measure the financial performance of an enterprise, the results of operations are ascertained by preparing an Income Statement (also called Profit and Loss Account) which shows the matching of current costs with current revenues during a particular accounting period. A systematic record of incomes and expenses facilitates the preparation of the Income statement.

To ascertain the financial position : To evaluate the financial strength and weakness of an enterprise, the financial position is ascertained by preparing a Position Statement (also called Balance Sheet) which shows resources (assets) owned by an enterprise and the sources of financing those resources.

A businessmen wants to know what the business owes to other and what it owns, and what happened to his capital whether the capital has increased, decreased or remained constant. A systematic record of various assets and liabilities facilitates the preparation of a Position statement (also known as Balance Sheet) which answers all these questions.

![]()

To communicate the information to the users : Accounting communicates information to internal users and external users. The internal users include all the organisational participants at all levels of management (i.e., top, middle and lower).

Top level management requires information for planning, middle level management requires information for controlling the operations. For internal use, the information is usually provided in the form of reports, for instance Cash Budget Reports, Production Reports, Idle Time Reports, Feedback Reports, Whether to Retain or Replace an Equipment Decision Reports, Project Appraisal Reports, and the like.

Since the external users (e.g., Banks, Creditors) do not have direct access to all the records of an enterprise, they have to rely on financial statements as the source of information. External users are basically interested in the solvency and profitability of an enterprise.

Question 3.

Enumerate main objectives of accounting?

Answer:

The following objectives of accounting may be preceded in brief:

1. Maintenance of Business Records : Accounting is the language in which most of the business transactions (financial) and events are expressed. It is an objective to keep a systematic record of these financial transactions. It embraces proper recording to – transactions, classified under appropriate accounts and summarised 1 into financial statements Income Statement and the Position Statement.

2. Calculation of Profit or Loss : Another objective of accounting is to ascertain the net result of the day-to-day transactions for a period. In other words, to ascertain whether during the period the firm earned a profit or suffered a loss. For this purpose, a statement called the Incomes Statement or the Profit and Loss Account is prepared.

In this account, the revenues resulting from the transactions of the period and the consequent expenses incurred are recorded. A comparison of the period and the consequent expenses incurred are recorded.

A comparison of the two shows whether the business earned a profit or incurred a loss. In addition, information is available about sales; opening and closing stocks of goods and the significant factors leading to the profit or the loss of the business.

Such a profit or loss statement is useful for all parties having stake in business like the management, lenders, investors, the proprietor or the partners or the shareholders, tax authorities and workers, etc. It is so because from its study, the management, can know whether the policies adopted by it were fruitful or not and can decide upon and possible, a change in the selling price or the advertising policy, etc.

![]()

Lenders can know from its study whether the firm is likely to earn profits in future also. Investors may also decide on its basis whether or not they should keep their money invested in the firm. Shareholders can make an estimate of the efficiency, success, etc., of the management and may decide accordingly whether to invest or not in the business.

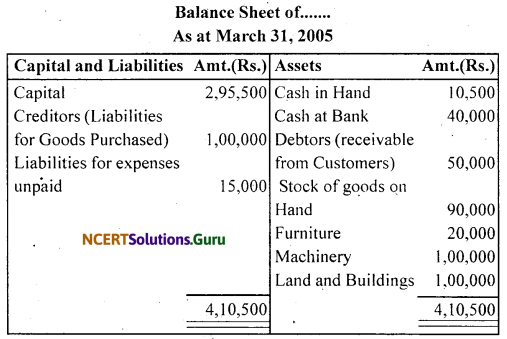

3. Depiction of Financial Position : For a businessman, it is not sufficient only to ascertain the profit & loss; it is also necessary to know the financial health of the firm. For this purpose, a statement listing assets, liabilities and the owner’s capital is prepared. Such a statement is called the Balance Sheet. An illustration of a Balance Sheet is as follows :

Just as a doctor will feel the pulse of a person and know whether he is enjoying good health or not, in the same manner by looking at the Balance Sheet one can know whether the firm is solvent or not. If the assets exceed liabilities, it is solvent. In the other case, it would be insolvent.

4. Provide information to various users : Making the information available to various groups and managers. This function of accounting is to communicate the financial facts about an enterprise to various interested parties like owners, investors, creditors, employees, government-offices, research scholar’s etc. The purpose of it is to enable these parties to take sound and realistic decision.

Question 4.

List any five users who have indirect interest in 7 accounting.

Answer:

Following are the interested parties or users of accounting informations other than the owners of a business :

1. Lenders: Lenders, i.e., the banks and financial institutions provide funds to the business. These funds may be provided at the time of setting-up the business or at a latter stage for the expansion and development. In practice, they lend money only after satisfying themselves about the repaying capacity, i.e., solvency of the ? business concern. Again, they know about this from the financial statements.

2. Managers : Managers have to take many decisions such as the determination of selling price, how can the cost be reduced, how 5 can the selling expenses and other expenses be controlled, etc. These decisions can be taken on the basis of the information available. This information is made available to them by the financial statements.

3. Government: The Government makes use of financial statements for compiling national accounts besides ascertaining the tax liability of the business, timely deposit of statutory and other dues.

4. Employees or Workers : Employees/workers may use the financial statements to know whether their dues like provident fund are being deposited regularly and also whether the bonus is being paid as per law.

5. Researchers : Last but not the least, the financial statements are of immense use to the researchers also undertaking researches in the typical areas like accounting theory, business affairs and practices.

Question 5.

State the nature of accounting information required by long-term lenders?

Answer:

In modem times, banks and financial institutions lend money f to the business; Before providing a loan to a business, they want to judge the repaying capacity of the business. Such information is provided by the accounting alone. Informations regarding the solvency of the financial business are made available only through statements. Financial statements help in assessing the financial capability of the business enterprise and also the expand to which the granting of credit will be safe.

![]()

Question 6.

Who are the external users of information regarding accounting?

Answer:

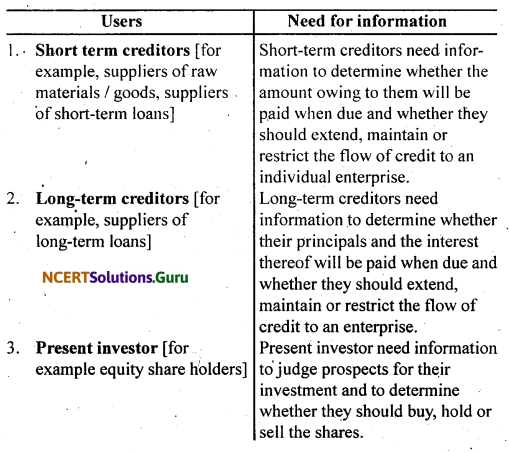

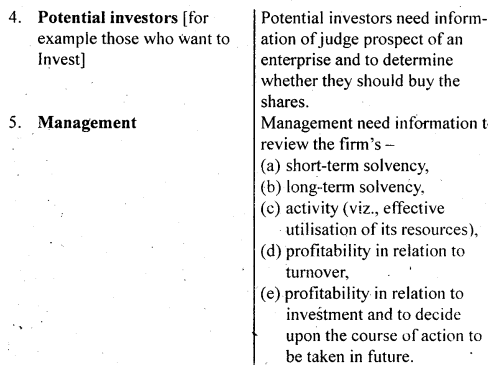

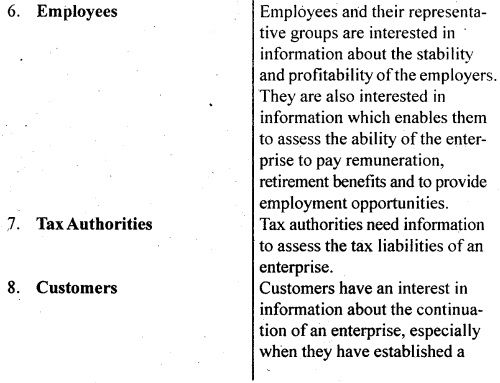

Users of Accounting Information and their Need : The users of accounting information include present and potential investors, management, employees, lenders, suppliers and other trade creditors, customers, government and their agencies and the public. These users use accounting information in order to satisfy some of their varied needs for information.

Question 7.

Enumerate informational needs of management.

Answer:

Management is interested to review the firm’s short-term solvency and long-term solvency, effective utilization of resources and profitability in relation to investments and turnover arid to decide upon the future course of action on the above decisions.

In addition to-the information about the profitability and financial soundness of business, management needs a lot of other informations for the efficient running of the business such as increase or decrease in sales, speed of increase in costs of production etc. All such informations are provided by the accounting which helps the management in planning, decision-making and controlling the business.

![]()

Question 8.

Give any three examples of revenues.

Answer:

Revenues are the amounts of the business earned by selling its products or providing services to customers, called sales revenue. Other items of revenue common to many businesses are:

- Commission

- Interest

- Dividends

- Royalties

- Rent received etc.

- Revenue is also called income.

Revenue in accounting is the income of a recurring (regular) nature from any source. It includes the amount received from sale of goods, rent receipt, commission, dividend and interest received. Any capital nature receipt is not a revenue item.

Question 9.

Distinguish between debtors and creditors.

Answer:

Following are the differences between debtors and creditors:

|

Debtors |

Creditors |

| 1. It represents those persons or firms to whom goods have been sold or services rendered on credit. 2. Payment has not been received from the persons or parties. 3. They still owe some amount to the business. |

1. It represents those persons or firms from whom goods have been purchased or services taken on credit. 2. Payment has not been made to the persons or parties. 3. Some money is still owing to them. , |

Question 10.

“Accounting information should be comparable.” Do you agree w’ith this statement. Give two reasons. .

Answer:

Comparability : Use must be able to compare the financial statement of an enterprise through time to identify trends in this financial position and performance. Users must also be able to compare the financial statements of different enterprise in order to evaluate their relative financial position, performance and changes in financial position.

Hence the measurement and display of the financial effect of such like transactions and other events must be carried out in a consistent way throughout an enterprise and over time for that enterprise and in a consistent way for different enterprises.

An important implication of this qualitative characteristic is that users be informed of the accounting policies employed in the preparation of financial statements, any changes in those policies and the effects of such changes so that users would be able to identify difference between the accounting policies for like transactions and other various events used by the same enterprise from period to period and by different enterprises, this qualitative characteristic requires pursuance of consistency in choosing accounting policies.

Lack of consistency may disturb the comparability quality of the financial statement information. Mere disclosure of accounting policies and changes therein may not be sufficient. Accordingly, accounting standard on disclosure of accounting policies consider consistency as a fundamental accounting assumption along with accrual, and going concern.

![]()

The basic reasons of comparing financial statement of two or more enterprises are the followings:

- Evaluating the financial position of different enterprise.

- Performance and changes in financial position of different firms.

- Accounting policies adopted by different firms.

Question 11.

If the accounting information is not clearly presented, which of the qualitative characteristics of the accounting information is violated?

Answer:

The qualitative characteristics of,both reliability and relevance are required to be followed so that truth and fairness of accounting informations be maintained. These may be explained in brief as follows:

Qualitative characteristics of Accounting information : The fundamental characteristics of the financial statement is truth and fairness. It means, Balance Sheet should give a true and fair view of the state of affairs and whereas the Profit and Loss Account should give the true and correct profit or loss for the period. Besides the above fundamental characteristics there are qualitative characteristics (attributes) that make the information content of the financial statements useful to its users.These are:

(i) Reliability;

(ii) Relevance.

(i) Reliability : An accounting information shall have the quality of reliability if it is free from material errors and also bias. The accounting information even if relevant can be of little use unless it is reliable also. Reliability of the information depends, on :

(a) Neutrality: Neutrality means that the accounting information made available does not suffer from bias. A biased accounting information will be misleading and lead to incorrect analysis and decisions.

(b) Prudence : The accounting information prepared on the principle of prudence (conservatism) means that the accounting information is prepared by providing all prospective losses while leaving all prospective profits. In other words, quality as to reliability increases if the accounting information does not paint a better picture than what actually is.

(c) Completeness : The accounting information given should be complete in all respects as incomplete

information may lead to wrong interpretation.

(d) Substance over form : The accounting information to be meaningful should be governed by the substance of the information and not by its legal form alone.

(ii) Relevance : The accounting information, besides disclosing statutorily required disclosures, should disclose other information, after judging its relevance to the decision making need of its users. For example, interest on borrowings is disclosed without stating the rate of interest. The users, therefore, cannot link interest cost to different types of borrowed funds. In the process, they fail to appreciate rationality of financing decisions. Generally, only the statutorily (legal) required information is disclosed.

The information disclosure requirements are set after a public debate reflecting the views of cross-sections of the users. But what is relevant information in a particular circumstance cannot be generalised and specified. It may be noted that relevance of the information is always guided by the principle of materiality.

![]()

Question 12.

The role of accounting has changed over the period of time. Do you agree? Explain.

Answer:

Today’s rapidly changing business environment has forced the accountants to reassess their roles and functions both within the organisation and the society. The role of an accountant has now shifted from that of a mere recorder of transactions to that of the member providing relevant information to the decision-making team. Broadly speaking, accounting today is much more that just book-keeping and the preparation of financial reports.

Accountant are now capable of working in exciting new growth areas such as forensic accounting (solving crimes such as computer hacking and the theft of large amounts of money on the internet), e-commerce (designing web-based payment system), financial planning, environmental account etc.

The realisation comes due to the fact that accounting is capable of providing the kind of information that managers and other interested persons need in order to make better decisions, this aspect of accounting gradually assumed so much importance that it was now been raised to the level of an information system.

As an information system, it collects data and communicates economic information about the organisation to a wide variety of users whose decisions and actions are related to its performance.

Question 13.

Giving examples and explain each of the following accounting terms:

(i) Fixed Assets

(ii) Gains

(iii) Profit

(iv) Revenue

(v) Expenses

(vi) Short-term liability

(vii) Capital

Answer:

Above-mentioned accounting terms may be explained as follows:

(i) Fixed Assets : Fixed assets refer to those assets which are held for the purposes of providing or producing goods or services and those that are not held for resale in the normal course of business. Fixed assets may be classified as follows:

- Tangible fixed assets : refer to those fixed assets which can be seen and touched. For example, Land and Building, Plant & Machinery and Furniture.

- Intangible fixed assets : refer to those fixed assets which cannot be seen and touched. For example, Goodwill, Patent, Trademarks, Copyrights etc.

(ii) Gains : Gains are increases in equity (not assets) from incidental transaction of an entity and from all other transactions and other events and circumstances affecting the entity during the accounting period except those that result from revenues or investment by equity participants. These gains may be operating or non-operating. Example 1 : Profit on sale of marketable securities is usually considered as operating gain.

Example 2 ; Profit on sale of a fixed asset is usually.considered as non-operating gain.

(iii) Profits: The excess of revenue of a period over its related expenses is accounting year profit. It is of two types:

- Net Profit : Net profit means the excess of revenue over expenses.

- Net Loss : Net loss means the excess of expenses and losses over revenue.

(iv) Revenue : The term ‘revenue’ refers to the amount charged for the goods sold or services rendered or permitting others to use enterprise’s resources yielding interest, royalty and dividend. For example, sales, commission earned, interest earned, royalty earned, dividend earned.

![]()

(v) Expenses : Expenses are decrease in economic benefits during an accounting period in the form of

- outflow or depletion of assets or

- incurrence of liabilities, that result in decrease in internal equity other relating to contribution from equity participant.

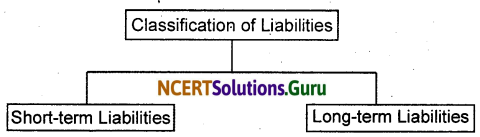

(vi) Liabilities : Liabilities refer to the financial obligations of an

enterprise other than owner’s funds. Liabilities may be broadly classified as follows:

- Current Liabilities/Short term Liabilities: Current liabilities refer to those liabilities which fall due for payment in a relatively short period, (normally, a period of not more than 12 months from the date of the Balance Sheet). For example, Bills payable, Trade Creditors, Outstanding Expenses, Bank. Overdraft and so on.

- Long-term Liabilities : Long-term liabilities refer to those liabilities which do not fall due for payment in a relatively short period. For example, Long-term loans.

(vii) Capital: Capital is the excess of assets over external liabilities. It refers to the amount invested in an enterprise by the proprietor (in case of proprietorship) or partners (in case of a partnership concern). This amount is increased by the amount of profits earned and amount of additional capital introduced and is decreased by the amount of losses incurred and the amount withdrawn (whether in the form of cash.or kind). It represents the owner’s claim on the assets of the enterprise. It is also known as owner’s equity or net assets or net worth.

Question 14.

How will you define revenue, expenses and income?

Answer:

Revenue : Revenue means the amount which, as a result of operations, is added to the capital. ‘Revenue is an inflow of assets which results in an increase in the owner’s equity.’ Examples of revenue are receipts from the sale of goods, rent, income, etc.

Expense : Expense is the amount spent in order to produce and sell the goods and services which produce the revenue. ‘Expenses is the cost of the use of things or services for the purpose of generating revenue.’ Examples are payment of salaries, wages, rent, etc.

Income : Income is the profit earned during a period of time. In other words, the difference between revenue and expense is called income. For example, goods costing Rs. 15,000 are sold for Rs. 21,000 the cost of goods sold, i.e., Rs. 15,000 is expense, the sale of goods, i.e., Rs. 21,000 is revenue and the difference, i.e., Rs. 6,000 is income.

It can, therefore, be expressed as: – Income = Revenue – Expense

Question 15.

What is the primary reason for the business students and other to familiarize themselves with the accounting discipline?

Answer:

In all activities whether business activities or non-business activities used by students of business and other interested groups like schools, colleges, hospitals, libraries, clubs, political parties etc. require accounting knowledge due to monetary transaction involved in these organisations. In other words, wherever money is involved or any economic activity is carried on, accounting is required to account for these economic resources. Accounting serves the basic purpose of information regarding flow of money and funds in the organisation. Following may be the reason for studying the accounting and familiarize with accounting discipline:

- Facilitates to replace memory.

- Facilitate to ascertain net result of operations.

- Facilitates the users to take decisions.

- Helpful in comparative study.

- Control over assets.

- Acts as legal evidence.

Long Answer Type Questions

Question 1.

Explain the factors which necessitated systematic accounting.

Answer:

Accounting is a systematic process of identifying the transactions of financial nature measuring them in money terms, recording in primary books, classifying, summarizing, analysis and interpreting and finally communicating the results to parties interested in them.

Following are the factors or attributes for systematic accounting records :

1. It records transactions of financial character : Accounting records only those events and transactions which are of financial character. If a transaction has no financial character then it cannot be measured in terms of money and thus, shall not be recorded in the books of account. It is a serious limitation of accounting. For example, a quarrel between the Production Manager and the Sales Manager affects the earnings of the business but it is not recorded because it has no financial character, no economic value and no exchange value.

2. It records transactions in terms of money: Accounting records the transactions by expressing them in terms of money. This makes the transaction more meaningful. For example, if a business has 10 machines, 20 tonnes of raw material, 2 buildings, 20 tables and chairs, 20 fans etc. it is not possible to add them together or know which one is more valuable unless they are expressed in terms of money.

![]()

3. It is an art: Accounting is that part of knowledge which enables us to achieve our objective of ascertaining the financial results by recording, classifying and summarising the business transactions.

4. It is an art of recording : Accounting is an art of recording ‘business transactions in the books of account in a systematic

manner soon after the occurrence thereof. Recording is carried out in the book called “Journal”.

This book may be further sub¬divided into various subsidiary books such as Cash Book (for recording cash transactions), Purchases Book (for recording credit purchases of goods), Sales Book (for recording credit sales of goods), Purchases Returns Book (for recording credit purchases returns), etc. The number of subsidiary books to be maintained . depends upon the size and nature of business and type of transactions.

5. It is an art of classifying business transactions : Classifying is the process of grouping of transactions or entries of one nature at one place. This is done by opening accounts in a book called ‘Ledger’, it contains all the accounts of the business. To get the correct idea of the net effect of transactions already recorded in a journal or subsidiary book they are further processed and grouped.

Similar transactions relating to a particular account for a given period are brought together. Then finally they are recorded at one place in a Ledger. For example, cash transactions like cash sales, cash purchases, cash expenses are put in one place in the Ledger under Cash Account.

Transactions pertaining to different persons, whether custonters or suppliers, are recorded separately in the name of each person in the Ledger. Likewise, all expenses under various heads after being recorded in the Journal are classified under separate titles in the Ledger.

6. It is the art of summarising the business data : Summarising is

the art of presenting the classified data (Ledger) in a manner which is understandable and useful to management and other interested parties. This involves preparation of final accounts which includes –

- Trading and Profit and Loss Account, and

- Balance Sheet.

Trading account is prepared for calculating gross profit or gross loss. Gross profit or gross loss is the difference’ between the cost of goods sold and sales. Profit and Loss Account is prepared to ascertain whether during the period the firm earned a profit or suffered a loss. Net profit increases owner’s capital and net loss decreases it.

After Trading and Profit and Loss Account, Balance Sheet is prepared to show the financial position of the business. Some people call it position statement also. The techniques of recording, classifying and summarising the transactions have been explained in detail later in the book.

7. It is helpful in the analysis and interpretation of the results:

For purposes of analysis, the accounting record must be in such a way as to be able to portray the significance of all transactions and events individually and collectively. Thus, the analysis of accounting statements will help the management to judge the performance of business operations and for preparing the future plans.The results of analysis and interpretations are communicated to the proprietor and other interested parties such as creditors, investors, employees, etc.

Question 2.

Describe in brief history of accounting.

Answer:

History and development of Accounting – The history of accounting is as old as civilization. Historical evidences reveal that accounting was 4000 B.C. old in Egypt as treasuries where gold and other valuables were kept. The incharge of treasuries had reported their superiors known as wazirs or Minister. Accounting practices in India could be traced back to a period when twenty three centuries ago, Kautilya. a minister in Chandergupt’s Kingdom wrote a book named Arthashashtra.

Lucas Pacioli, an Italian writer first wrote a book on Double entry in 1494.

This book contains knowledge of business and book-keeping. Contents of the book even relied in current accounting world as the popular terms Debit (Dr.) and Credit (Cr.), while preparing accounts of a business enterprise. These concepts were used in Italian terminology. Debit comes from the Italian word Debito or debeo which means owed to the proprietor, credit comes from the Italian word Credito or credo which means trust or belief in the proprietor.

In explaining double entry system Pacioli wrote that “All entries have to be double entries that is if you make one creditor, you must make some debtor.” He also stated that a merchant’s responsibility include to give glory to God in their enterprise, to be ethical in all business activities and to earn a profit. He discussed the details of memorandum, Journal, ledger and specialised accounting practice. Today the accounting information’s plays a vital role in a business enterprise.

![]()

Question 3.

Explain the development and role of accounting.

Answer:

A sound theory is the base for development of any discipline. Accounting assumes importance because the financial statements are useful to a number of users such as owners, investors, creditors, lenders, Government etc. Accounting is the language of business, it means that an enterprise communicates with the outside world, including the proprietors through accounting statements. One cannot understand the affairs of an enterprise unless the enterprise prepares financial statements intelligently.

Following are the reasons assisted in the development of accounting as a separate discipline :

1. Assistance to Management : Accounting, in addition to ascertaining the financial results of operations, also performs the significant function of providing information. The information provided enables the management to arrive at a decision and to do it’s work properly. Such information helps in the following:

(a) Planning : Management would like to estimate the sales, output, expenses, etc. For the following year and also the flow of cash. For this purpose, accounting would enable them to collect the necessary information and make the realistic estimates.

(b) Decision-Making : Management is faced at a times, with a number of problems requiring an appropriate decision. For example: What should be the selling price of goods produced? Should a concession be offered to a special customer and, if so, how much? Should a part be made in the factory or purchase from outside? For making such decisions only accounting can provide the relevant information.

(c) Controlling : Management would like to see that –

- the work is performed according to the plan, and

- the cost incurred is reasonable.

Accounting collects information to help management in this regard. For instance, management would be able to know which department is overspending.

2. Replacement of Memory : No businessman can remember everything about his business since memory has limitations. It is necessary to record transactions in the books of account promptly. This will obviate the necessity of remembering the various transactions since on need, the record will furnish the necessary information.

3. Comparative Study : A systematic record will enable a businessman to compare one year’s results with those of other . years and locate significant factors leading to the change, if any.

4. Settlement of Taxation Liability : If accounts are maintained properly, they will be of great assistance when the firm is assessed to income tax or sales tax.

5. Evidence in Court: Systematic record of transactions is often treated by the Courts as good evidence.

6. Sale of Business : If someone desires to sell his business, the accounts maintained by him will enable the ascertainment of the proper purchase price.

7. Assistance to an Insolvent Person : In case one becomes insolvent, one has to explain many things about the past. Proper accounting helps him to do that.

Question 4.

Define Accounting and state its objectives.

Answer:

Accounting : Accounting refers to the actual process of preparing and presenting the accounts, in other words, it is the art of putting the academic knowledge of accountancy into practice. It covers the following activities :

1. Identifying the transactions and events.

2. Measuring the identified transaction and events in a common measuring unit.

3. Recording the identified and measured transactions and events 1 in Journal.

4. Classifying the recorded transactions and events in ledger.

5. Summarising the classified transactions and events in the form

of Income Statement and Position Statement.

6. Analysing the summarised results,

7. Interpreting the analysed results.

8. Communicating the interpreted information of the interested ‘ parties.

Objectives or Functions of Accounting :

The following are the main objectives, functions or utility of accounting:

(1) To keep systematic record of business transaction : The main objective of accounting is to keep complete record of business transactions according to specified rules. Complete record of business transaction helps to avoid the possibility of omission and fraud. For this purpose, all the business transactions are first of all recorded in Journal or Subsidiary Books and then posted into Ledger.

(2) To calculate profit or loss : The second main objective of accounting is to ascertain the net profit earned or loss suffered on account of business transactions during a particular period for this purpose trading and profit and loss account of the business is prepared at the end of each accounting period. All the items relating to purchases, sales, expenses and revenues (incomes) of the business are recorded in trading and profit & loss account. If the amount of revenue exceeds the expenditure incurred in earning that revenue, there is said to be a profit. In case the expenditure exceeds the revenue, there is said to be a loss. In addition, a businessman is able to get the following informations by preparing a trading and profit & loss account:

![]()

- How much goods have been purchased during a particular period.

- How much goods have been sold during a particular period.

- How much goods have remained unsold and what is its value.

- How much amount has been spent on various heads of expenditure and how much amount has been earned by various heads of revenues.By attaining these informations a businessman can keep effective control on expenditure.

(3) To know the exact reasons leading to net profit or net loss.

(4) To ascertain the financial position of the business : For a businessman, merely ascertaining profit or loss of the business is not sufficient. The businessman must also know the financial health of the business. For this purpose, after preparingthe Profit & Loss Account a statement called ‘Balance Sheet’ is prepared which shows the assets and their values on the one hand and the liabilities and capital on the other hand. A Balance Sheet is actually a screen picture of the financial position of the business. At one glance, one would know the following by looking at the Balance Sheet:

- How much the business has to recover from Debtors.

- How much the business has to pay to Creditors.

- How much the business has in the form of –

(a) Cash in hand

(b) Cash at Bank

(c) Closing Stock, and

(d) Fixed Assets.

(5) To ascertain the progress of the business form year to year.

(6) To prevent and detect errors and frauds.

(7) To provide informations to various parties : Another main objective of accounting is to communicate accounting information to various interested parties like owners, investors, creditors, banks, employees and government authorities etc. The information helps them in taking sound and judicious decisions about the business entity.

Question 5.

Describe the informational needs of external and internal users. .

Answer:

Accounting as an Information System : Accounting is often regarded as the language of business. Since the main aim of a language is to serve as a means of communication, accounting communicates the result of business activities to management, owners, investors, creditors, lenders, Government etc.

Accounting as an information system is a process of identifying, measuring, recording, summarising and communicating the information about business to interested users of such information. Different groups of persons have vested interests in a business organisation. Accounting provides useful information to all these interested parties. Following Parties are interested in Accounting Information :

(1) Management : In addition to the information about the profitability and financial soundness of the business, management needs a lot of other informations for the efficient running of the business such as increase or decrease in sales, speed of increase in the cost of production etc. All such informations are provided by the accounting which helps the management in planning, decision making and controlling the business.

(2) Owners : Owners want to know about the profitability and financial soundness of the business. They also want to know whether the profits are increasing or decreasing. What are the reasons for the increase or decrease in profits? What is the value of fixed assets and floating assets of the business? All such information is provided by accounting.

![]()

(3) Investors : Investment of money in a business enterprise involves risk. Hence, those who want to invest money in a business enterprise need, information to judge how safe and rewarding the proposed investment will be. The financial statements, i.e., accounting provides them such information. On the basis of such information they decide whether to become a partner in a firm or whether they should buy, hold or sell the shares of a company..

(4) Creditors: Creditors are the persons who supply goods or services on credit. Before granting credit, creditors want to be satisfied about the creditworthiness of the business enterprise. Financial statements help them in assessing the financial capability of the business enterprise and also the extent upto which the granting of credit will be safe.

(5) Lenders : In modern times, banks and financial institutions lend money to the business. Before providing a loan to a business, they want to judge the repaying capacity of the business. Such information is provided by the accounting alone.

(6) Employees : Employees need information about the profits of a business to assess the ability of the business to pay higher wages and bonuses. They may also use the financial statements to ascertain whether various amounts due to them such as provident fund is being deposited regularly.

(7) Government : The Government is interested in the financial statements of a business on account of assessment of income tax, sales tax, excise duty etc. As such, the Government wants that the accounts are maintained in a true and fair manner.

Question 6.

What do you understand by an Assets and what are different types of assets?

Answer:

Assets: Anything which is in the possession or is the property of a business enterprise including the amounts due to it from others, is called an asset. In other words; anything which will enable a business enterprise to get cash or a benefit in future is an asset. Thus, Cash and Bank balances, Stock, Furniture, Machinery, Land and Building, Bills Receivable, Money owing by Debtors etc., are all assets.

Assets arefuture economic benefits, the rights of which are owned or controlled by an organisation or individual. – Finney & Miller

“Assets are valuable resources owned by a business which are acquired at a measurable money cost. ” – Prof. R.N. Anthony

According to the above definitions there are three main characteristics to an asset:

- The resources must be valuable.

- The resources must be owned by the business.

- The resources must be acquired at a measurable money cost. Assets may be classified into the following categories :

(i) Fixed Assets : Fixed assets refer to those assets which are held for continued use in the business for the purpose of producing goods or services and are not meant for resale. Examples of fixed assets are:

Land and Building, Plant and Machinery, Motor Vehicles, Furniture etc.

(ii) Current Assets : Current assets are those assets which are meant for sale or which the management would want to convert into cash within one year. As such, these assets are also named as ‘short-lived or active assets’. For example, ‘Debtors’ are expected to be converted into cash within a reasonable short period, Stock is continuously sold and Bills receivables are also converted into cash.

According to the Institute of Certified Public Accountants, U.S.A “Current assets include cash and other assets or resources commonly identified as those which are reasonable expected to be realised in cash or sold or consumed during the normal operating cycle of the business.” Although ‘Prepaid Expenses’ will never be realised in Cash, these are also included in Current Assets, since service or benefit will be available against these without further payment.

![]()

Current assets are also known as floating assets or circulating assets as the amount and nature of such assets keeps changing continuously. For example, a businessman purchases goods for cash and these goods are sold to X. X becomes our debtors and it means that the stock has been converted into Debtors. Again, if a bill receivable from X, it means that the bills are converted into ‘Bills Receivable’ and after some time Bills Receivable will be converted into cash. It shows that all Current assets are finally converted into Cash.

Current assets are usually shown in the balance sheet in the ‘Liquidity Order’. Liquidity is the facility with which the asset may be converted into cash. Those assets which are most difficult to be converted into cash are written lost. Following are the current assets in order of liquidity : Cash in Hand, Cash at Bank, Bills Receivable, Short-term Investments, Debtors, Stock and Prepaid Expenses.

Out of the above assets, Stock and Investments are shown in the balance sheet at Cost or Market price whichever is less. Bills Receivable and Debtors are shown at the estimated realisable . values and the Cash in Hand and Cash at Bank are shown at the actual figure.

(iii) Tangible and Intangible Assets : Tangible assets are those assets which can be seen and touched. In other words, which have a physical existence such as Land, Building, Plant, Furniture, Stock, Cash etc. Intangible assets are those assets which do not have a physical existence and which cannot be seen or felt.

Examples of such assets are Goodwill, Patents, Trade Marks and Prepaid expenses. Intangible assets are also valuable assets. For example, with the help of patent rights businessman is able to produce goods and his goodwill helps in attracting customers easily. Therefore, the intangible assets help the firm in earning profits as much as the tangible assets.

Question 7.

Explain the meaning of gain and profit. Distinguish between these two terms.

Answer:

Profit : The excess of revenue of a period over its related expenses during an accounting year is called profit. Profit increases the investment of the owners. Surplus of revenue over expenses is also known as Profit. For example, the goods costing Rs. 5,00,000 are sold for Rs. 6,50,000. The sale amount of Rs. 6,50,000 is the revenue and Rs. 5,00,000-cost of goods purchased is the expense and the surplus amount of Rs. 1,50,000 is the accounting profit.

Gain : A profit that arises from events or transactions which are incidental to business such as sale of fixed assets, winning a Court case, appreciation in the value of assets is known as Gain. For example if a building costing Rs. 5,00,000 is sold for Rs. 6,00,000, Rs. 1,00,000 will be gain on sale of building.

The only difference between Profit and Gain is the source of revenue earned. The profit is the amount of excess of income over expenditure, w’here as the amount of gain is the result of transactions incidental to business other than operating transactions.

Question 8

Explain the qualitative characteristics of accounting information.

Answer:

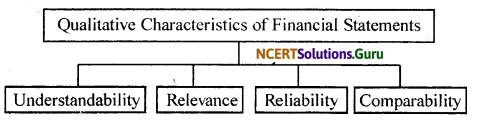

Qualitative characteristics of financial statements :

Qualitative characteristics are the attributes that make the information provided in financial statements useful to users.

The four principal qualitative characteristics are:

Let us discuss these qualitative characteristics one by one :

1. Understandability : An essential .quality of the information provided in financial statements is that it is readily understandable by users. For this purpose, users are assumed to have a reasonable knowledge of business and economic activities and accounting and a willingness to study the information with reasonable ‘ diligence.

However, information about complex matters that should be include in the financial statements because of its relevance to the decision-making needs of user should not be excluded merely on the grounds that it may be too difficult for certain users to understand.

2. Relevance : To be useful, information must be relevant to the decision-making need of users. Information has the quality of relevance when it influences the economic decisions of the users by helping them to evaluate past, present or future events or confirming or correcting their past evaluation.

The productive and confirmatory roles of information are interrelated. For example, information about the current level and structure of asset-holding has value to users when they endeavour to predict the ability of the enterprise to take advantage of opportunities and its ability to react to adverse situations.

![]()

The same information plays a confirmatoty role in respect of past prediction about, for example, the way in which the enterprise would be structured or the outcome of planned operations.

Materiality: The relevance of information is affected by its nature and materiality. Information is material if its omission or mis-statement could influence the economic decisions of users made on the basis of financial statements. Materiality depends on the size of the item or error judged in the particular circumstance of its omission or mis-statement. Thus, materiality provides a threshold or a cut-off point rather than being a primary qualitative characteristic which information must have if it is to be useful.

3. Reliability : To be useful, information must also be reliable. Information has the quality of reliability when it is free from material error and bias and can be depended upon by users to represent.

Faithfully that which it either purpose to represent or could reasonable be expected to represent. Information may be relevant but so unreliable in nature or representation that its recognition may be potentially misleading and so it becomes useless.

Reliability of the financial statements is dependent on the following:

(i) Faithful representation : To be reliable, information must represent faithfully the transactions and other events which either purports to represent or could reasonably be expected to repeat. Most financial information is subject to some risk of being less than a faithful representation of that which it purports to portray. This is not due to bias but rather to enhance difficulties either in identifying the transactions or other events to be measured in devising or applying measurements and presentation techniques that can convey messages that correspond with those transaction and events.

(ii) Substance over form : If information is to represent faithfully the transactions and other events that it purports to represent, it is necessary that they are accounted for and presented in accordance with their substance and economic reality and not merely by their legal forms. The substance of transactions or other events is not always consistent with that which is apart from their legal or contrived form.

(iii) Neutrality : To be reliable the information contained in financial statements must be neutral. Financial statements are not neutral if by selective presentation of information, they influence the making of a decision or judgement in order to achieve a predetermined result or outcome.

(iv) Prudence : The preparers of financial statements have to contend with uncertainties that inevitably surround many events and circumstances. Such uncertainties are recognised by the disclosure of their nature and extent and by exercise of prudence in the financial statements. Prudence is the inclusion of a degree of caution.

In the exercise of judgement needed in making the estimate required under conditions of uncertainties so that assets or income are not overstated and liabilities or expenses are not understated. However, the exercise of prudence does not allow the creation of hidden reserves or excessive provisions, the deliberate understatement of assets or income or deliberate over statement of liabilities or expenses.

(v) Completeness : To be reliable the information in the financial • statements must be complete within the bounds of materiality and cost. An omission can cause information to be false or misleading and thus, unreliable and deficient in terms of its relevance.

4. Comparability : Comparability means that the users should be able to compare the accounting information of an enterprise of the period either with that of other’periods, known as intra-firm comparison or with the accounting information that of other enterprises, known as interfirm comparison. It is, therefore, necessary to follow standardised accounting policies consistently to the extent possible.

Accounting measurement and treatment of any transaction depends, to a large extent, on the nature of the enterprise, conditions of the occurrence of transactions and the legal frame work. It is, therefore, difficult to follow one single accounting policy for recording a transaction or an event. To uphold the quality of comparability, it is necessary to disclose the accounting policies followed in relation to all important elements of financial statements. In case the enterprise switch over from one policy to another, the effect of such change should be quantified and disclosed.

In practice, it has also become necessary to achieve an appropriate balance among the qualitative characteristics in order to meet the objective of financial statements. Assessment of the relative importance of the characteristics is a matter of professional judgment.

Question 9.

Describe the role of accountant in the modern world.

Answer:

Role of an accountant in the society: An accountant with his education, training, analytical mind and experience is best qualified . to provide multiple need-based service to the end growing society The accountants of today can do full justice not only to matters relating to taxation, costing, management accounting, financial layout, company legislation and procedures but they can act in the fields relating to financial policies, budgetary policies and even economic principles, the services rendered by accountants to the society include the following:

(a) To maintain the Books of Accounts in a systematic manner

(b) To act as a Statutory Auditor (for example under the Companies Act, Income Tax Act, Co-operative Societies Act)

(c) To act as an Internal Auditor

(d) To act as Social Auditor

(e) To act as Taxation Adviser

(f) To act as Management Accountant

(g) To act as Financial Advisor

(h) To provide Management Consultancy Services

(i) To act as Company Law Advisor

(j) To act as Liquidator

(k) To act as Arbitrator

(l) To act as Receiver

(m) To act as Management Information System Consultant.

![]()